If you are a UAE resident, especially an expatriate, you know the importance of remittance especially during the festive season. From buying gifts to planning travel and celebrations, your loved ones back home depend on the money you send to meet these expenses.

It is your hard-earned money that makes all of this possible. The money you send home helps your loved ones celebrate, plan, and smile a little more during the festive season. Naturally, this is also the time when more people send money, and remittance costs tend to rise.

This article will help you make smarter decisions to ensure your loved ones receive the most from the money you send, without compromising on speed or security.

What Is Remittance and Why It Matters During the Festive Season

Remittance as you know refers to the process of transferring money from one person to another most often by those living or working abroad to support their families or loved ones back home.

For millions of UAE residents, international remittances play a vital role in covering everyday expenses such as education, medical needs, household costs, and special celebrations.

So, why does remittance matter most during the festive season?

Festive seasons bring with them add-ons such as festival preparations, buying gifts, planning travel, and creating memorable moments. To meet these needs, families back home rely more on the money you send. As a result, remittance volumes naturally increase during festive periods.

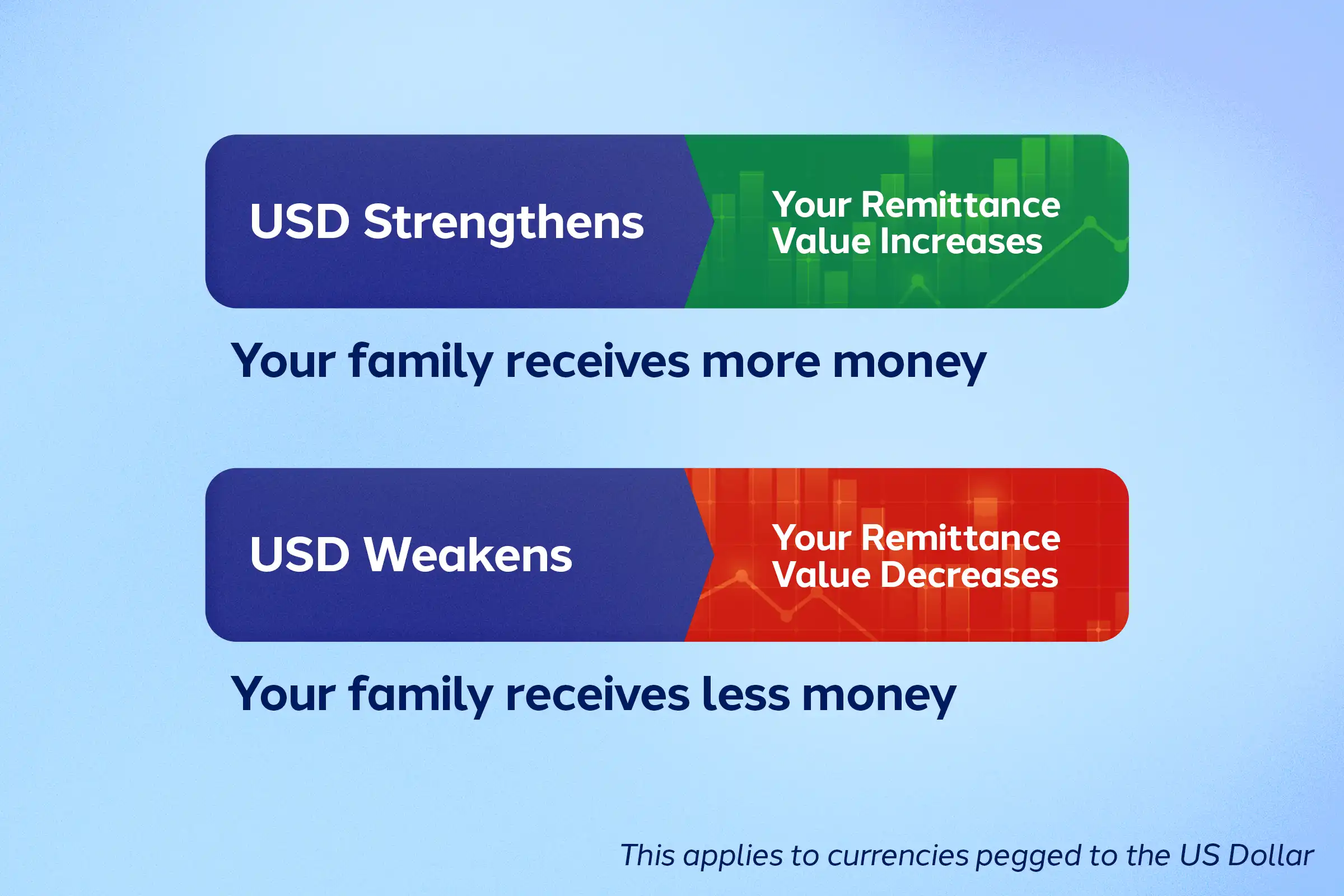

When more people send money at the same time, transfer fees and exchange-rate costs often rise as well. So, it’s important that you save on these remittance costs especially during the festive season.

Smart Ways to Save on Remittance Fees During Festive Season

1. Compare Providers, Don’t Default to Your Bank

Traditionally, banks were the first choice for international money transfers. But banks often charge higher fees and apply wider exchange-rate markups, especially around peak seasons.

What you can do instead are:

- Choose exchange houses or remittance apps.

- Compare the exchange rates & processing times across different platforms.

2. Use Digital Remittance Apps

Digital remittance apps have completely transformed how UAE residents send money internationally.

They often offer:

- Competitive exchange rates

- Lower or discounted transfer fees

- Faster processing times

- Clear, transparent pricing

Not just that! Most of these providers run festive-season offers, thus making digital channels one of the most cost-effective ways to send money home. With apps like LuLu Money, you can send money quickly at competitive rates and clear fee visibility.

3. Plan Ahead and Time Your Transfers Wisely

If you want to save more, you should:

- Avoid last-minute transfers

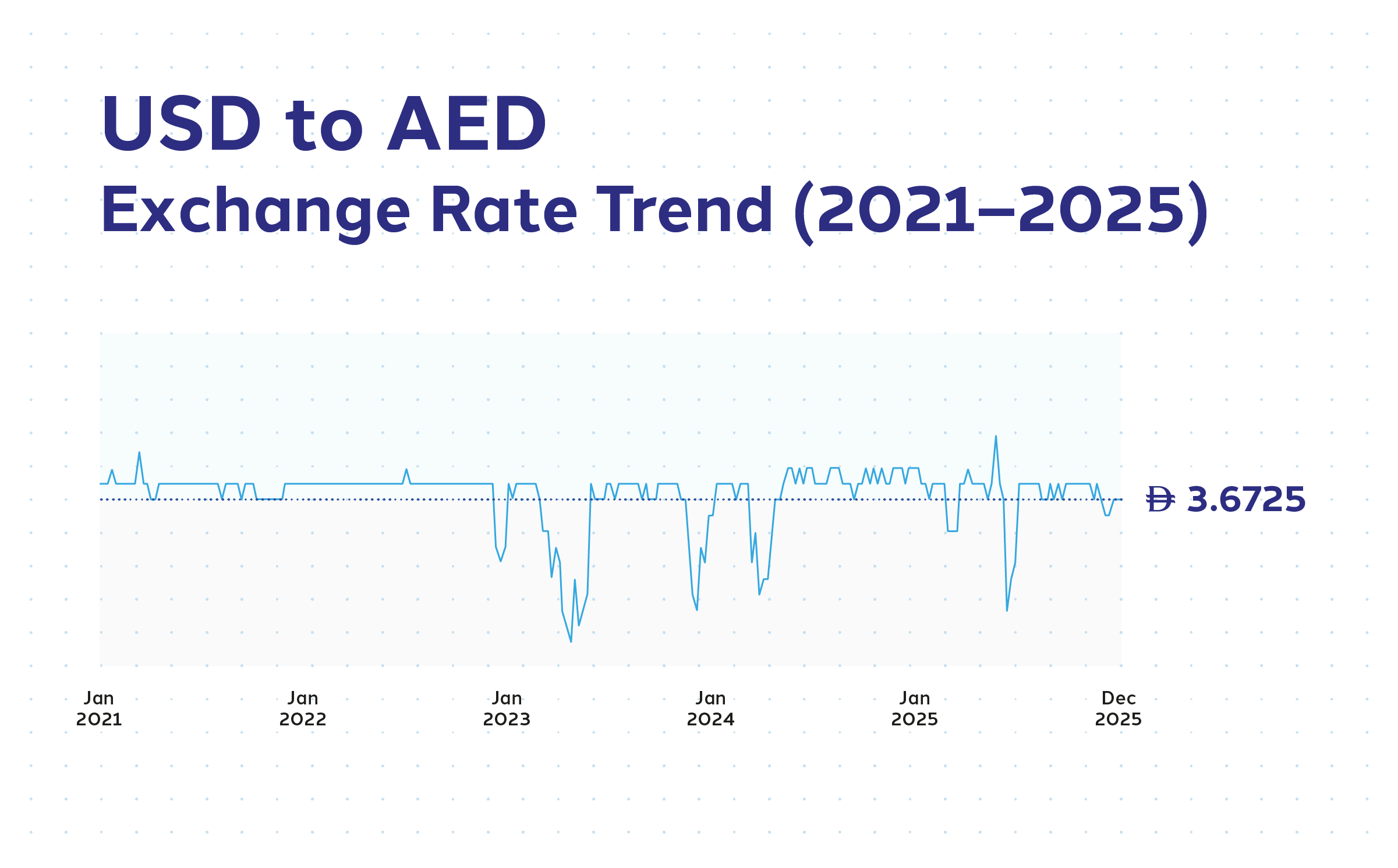

- Regularly monitor exchange rate trends

- Transfer when the rates are the most favourable

Planning ahead helps you avoid poor rates and unnecessary fees.

4.Compare the Actual Cost, Not Just the Fee

A low transfer fee doesn’t always mean a cheaper transfer. Some services compensate by offering less favourable exchange rates or adding hidden charges.

So, before sending money:

- Compare the rate with the market rate

- Confirm the final amount your recipient will receive

Transparency is key to real savings.

Check out the best time to send money from the UAE to India!

5. Watch Out for Festive Offers and Rewards

Festive seasons are the peak time for promotions.

Most remittance providers offer:

- Reduced or zero transfer fees

- Better exchange rates

- Cashback or reward points

Always keep an eye on these offers that can help you save the most.

6. Avoid Hidden Charges

Some transfers come with hidden or unexpected costs that reduce the amount your loved ones finally receive.

These may include:

- Correspondent bank fees

- Receiving bank deductions

- Charges applied due to weekend or holiday processing

- Unlike traditional methods, most digital platforms offer transparent pricing.

With apps like LuLu Money, you know exactly how much you’re sending and how much your family will receive, with no surprises later.

7. Consolidate Transfers Where Possible

If you are someone who send money frequently, then:

- Combine multiple small transfers into one

- Use recurring transfer options when available

- Plan monthly or festive transfers in advance

This helps reduce repeated fees and maximises value.

Keep yourself informed about the common money scams around you!

Final Thoughts

The festive season is about joy, connection, and togetherness, not unnecessary remittance costs. By understanding remittance, comparing providers, using digital platforms, and planning your transfers wisely, UAE residents can save significantly on fees while ensuring timely support for their loved ones.

With the right approach, you can make every transfer count, keeping more money where it truly belongs: with your family back home.

Frequently Asked Questions (FAQs)

Why do remittance fees increase during the festive season?

During the festive season, remittance volume will be higher, and it is this increased demand that leads to increased fees and less favourable exchange rates.

Are digital remittance apps cheaper than banks?

Yes, digital remittance apps usually offer better exchange rates and lower fees compared to traditional bank transfers.

How can I ensure my family receives most of the money I send?

Compare providers, choose transparent platforms, and avoid last-minute transfers to reduce unnecessary costs.

Is it safe to send money through digital remittance apps?

Yes, authorised digital remittance apps follow strict security and regulatory standards to keep your transfers safe.

Can money be transferred instantly during the festive season?

Yes, many digital remittance apps offer instant or near-instant transfers, even during peak festive periods.